- The World Trade Organization (WTO) remains the backbone of global trade and is being modernized, not sidelined, despite what its critics say.

- The WTO’s emerging framework for data flows, algorithmic transparency and digital standards could replace a patchwork of national regimes with interoperable rules.

- A reform agenda within WTO will reshape supply chains by integrating small- and medium-sized businesses and sustaining open markets.

Despite ongoing challenges to global cooperation, there is a reality in global trade which every CEO will agree upon: global commerce still needs a credible multilateral anchor.

Over the past decade, the World Trade Organization (WTO) has faced challenges in policy discussions, with some perceiving it as struggling to adapt to modern trade dynamics and instead being overtaken by bilateral deals and hamstrung by geopolitics. They believe its role has diminished in an economy largely driven by data, artificial intelligence (AI) and digital services.

But the reality could not be more different. According to the WTO, about 72% of global goods trade still takes place under its default tariff rules.

Customs procedures, transparency standards and market-access guarantees all derive from this architecture. Without it, we risk deepening fragmentation and commercial outcomes dictated by geopolitics.

Have you read?

- We can still save the World Trade Organization. Here’s how

- Global trade needs AI and leaders willing to invest despite uncertainty

- New Economy Skills: Building AI, Data and Digital Capabilities for Growth

How the WTO is reforming

The WTO is quietly undergoing the most significant transformation in its 30-year history. The regulatory frameworks emerging from this reform will determine competitive advantage, market access and regulatory risk for every globally exposed business.

There are three structural forces that are informing the WTO reform agenda:

1. AI is now central to trade policy

AI is redefining manufacturing, finance, logistics and professional services. According to the WTO’s World Trade Report 2025, AI could lift global exports by up to 40% above trend by 2040.

WTO Director-General Ngozi Okonjo-Iweala simultaneously cautions: “Access to AI technologies and the capacity to participate in digital trade remain highly uneven.”

The hope is that the WTO’s efforts to establish interoperable standards for data flows, algorithmic transparency and liability will lead to a unified regulatory framework rather than having to navigate 164 separate regimes, each with different standards.

The differences in compliance costs, time-to-market and legal exposure are measured in the billions.

Cloud service providers, fintech platforms and AI-driven logistics firms are already navigating conflicting data localization requirements across jurisdictions – a problem that harmonized WTO rules could resolve.

The WTO’s emerging AI framework would determine whether cloud infrastructure investments are economically viable, whether cross-border data flows remain predictable and whether smaller competitors can access the same digital tools as incumbents.

2. SME integration reshapes competitive dynamics

Small and medium-sized enterprises represent 90% of global firms, yet they remain underrepresented in international trade, accounting for only 34% of global exports despite their numerical dominance.

Simplified documentation, digitized processes and reduced compliance costs could integrate millions into global value chains – driving competitiveness and resilience across industries and economies.

The WTO’s reform agenda explicitly prioritizes digital trade facilitation, reducing customs timelines from weeks to hours. It focuses on simplified regulatory compliance to make exports economically viable for smaller players; transparent access to global value chains; and support for women- and youth-led enterprises.

For large multinationals, this means access to more agile, specialized suppliers and new partnership opportunities. For SMEs, it means reduced barriers to competing globally. Either way, the competitive landscape is shifting and companies that anticipate it gain a first-mover advantage.

The WTO is imperfect but it remains essential in anchoring a global economy shaped by AI, digital services and geopolitical rivalry.

3. Sustained growth still requires open markets

Amid headlines about “friend-shoring,” reshoring and supply chain nationalism, a fundamental economic truth persists: no major economy has achieved sustained growth through protectionism.

Dr Okonjo-Iweala made this case forcefully at the World Economic Forum’s Annual Meeting 2024 in Davos, Switzerland: “We need to think of globalization differently… The reason [is] because poor people in rich countries were left out and poor countries or developing countries were at the margin. In the new paradigm, we don’t want to repeat the same story.”

The WTO’s modernization will:

- Directly affect the ability of businesses to enter new markets without negotiating bilateral agreements with 166 different member nations.

- Resolve trade disputes through established mechanisms rather than retaliatory tariffs.

- Plan long-term capital investments with regulatory certainty and access global talent and innovation clusters without bureaucratic friction.

The institution’s dispute settlement system – currently paralyzed – once provided a neutral forum for resolving trade conflicts. Without it, subsidies proliferate unchecked, market access barriers persist and commercial outcomes increasingly hinge on political leverage rather than legal merit.

Why reform remains difficult

Structural and political challenges persist. Consensus-based decision-making can entrench gridlock. Large economies continue to adopt unilateral tariffs and industrial policies.

New areas – including AI governance, data protection and sustainability – require complex rulemaking. Subsidies are expanding across sectors, complicating any effort to maintain a level playing field.

Yet the institution’s imperfections do not reduce its importance. A fractured world cannot manage AI standards, climate-linked trade measures, cross-border digital services or supply-chain shocks through bilateral deals alone. These issues require multilateral governance.

A logo is pictured on the headquarters of the World Trade Organization (WTO) in Geneva, Switzerland, June 2, 2020Image: REUTERS/Denis Balibouse

What business should do

Jens Lund, CEO of DSV, the world’s largest freight forwarding company, noted in October 2025: “In a world of geopolitical turbulence, trade tensions and climate disruptions, supply chains thrive not by avoiding trouble but by anticipating it.”

In this regard, business leaders should treat WTO reform as a strategic issue:

- Engage through industry associations to shape emerging rules.

- Build regulatory scenario planning into strategy, including scenarios of deeper fragmentation or renewed multilateralism.

- Diversify suppliers, especially as SMEs gain tools to enter global value chains.

- Monitor dispute settlement talks, which will determine whether the system regains credibility.

Firms that participate in rulemaking will benefit from foresight and stability. Those that ignore multilateral processes will face rising compliance costs and strategic uncertainty.

The WTO is imperfect but it remains essential in anchoring a global economy shaped by AI, digital services and geopolitical rivalry. The question is not whether the WTO is obsolete. It is whether the world can afford a future without it.

- September marks 20 years since the Logistics Emergency Team was established to support humanitarian aid efforts across the globe.

- More than 305 million people require humanitarian aid, according to the latest data.

- Worsening humanitarian crises around the world further highlight the need for public-private sector coordination in aid efforts.

The world faces an unprecedented humanitarian crisis. With conflicts raging in Ukraine, Gaza and Sudan, among other places, and climate disasters striking with increasing frequency, the need for coordinated aid delivery has never been more urgent.

The latest data shows more than 305 million people are in need of aid, requiring $47.4 billion in funding.

One pioneering partnership involved in the complex relief operations worldwide is the Logistics Emergency Team (LET), which turns 20 this year. Here’s what to know about the LET and the importance of fostering public-private partnerships to deliver aid.

In 2005, the United Nations Cluster Approach was introduced to bring together fragmented relief efforts. Included in the initiative was the World Food Programme (WFP)–led Logistics Cluster, which recognized that strong coordination is necessary for any successful emergency response.

For the past 20 years, leveraging the capabilities of WFP as the largest humanitarian agency in the world, the Logistics Cluster has been the backbone of humanitarian operations, coordinating supply chains, filling common gaps and enabling other organizations responding to an emergency to reach people in need.

That same year, the World Economic Forum convened four of the world’s leading logistics companies—Agility, UPS, Maersk and DP World—to create the Logistics Emergency Teams (LET). LET was the first public–private partnership of its kind in the humanitarian space, with the four companies joining forces to provide pro bono support to the humanitarian sector upon request from the Logistics Cluster.

The LET was designed with a simple but powerful logic: by supporting the Logistics Cluster, private sector expertise and assets could support the entire humanitarian system.

“Maersk is proud to work alongside our industry peers and international organizations, contributing our assets and expertise to the LET,” said Lene Bjørn Serpa, Director and Head of Corporate Sustainability at A.P. Moller – Maersk. “Effective logistics support is critical in an emergency, and the LET is a prime example of how public-private partnerships can support more effective disaster response and preparedness activities and bring critical humanitarian aid where it is needed the most.”

Research shows that without coordination and collaboration, humanitarian logistics can remain fragmented and inefficient. In fact, a 2018 study by Help Logistics Ag, Kuehne Logistics University and Save the Children International found that up to 73% of humanitarian spending is tied to supply chains.

“When disaster strikes, logistics saves lives,” said Nikki Clifton, President, Social Impact and The UPS Foundation. “The UPS Foundation is proud to work with our LET partners to help vulnerable communities prepare, respond, and recover. Together, we are accelerating relief and improving access to essential resources until recovery becomes resilience.”

Operating as a force multiplier for humanitarian response, the LET works with the Logistics Cluster to provide warehousing, transport, customs clearance expertise and logistics specialists to fill critical gaps in humanitarian supply chains.

The partnership deploys upon request from the Logistics Cluster, which today leads a global community of more than 1,150 partner organizations, with 50% being national actors.

“At DP World, we know resilient communities build resilient business,” said Ayla Bajwa, Group Senior Vice President, Group Sustainability, DP World. “That’s why we partner with fellow LET companies—to combine our global strengths and deliver fast, coordinated humanitarian response. Together, our supply chains become lifelines when it matters most.”

One of the LET’s most innovative contributions is EDUARDO, the Emergency Dashboard Utility for Airfreight Resource and Delivery Options, which uses Google flight data to identify available cargo capacity for humanitarian operations. During the Türkiye-Syria earthquake response in 2023, EDUARDO was accessed 510 times in its first month, demonstrating its critical value in rapid response scenarios.

“Logistics is the backbone of every emergency response. But it’s partnerships that power the response,” said Stefano Peveri, Global Logistics Cluster Coordinator. “The LET brings together the agility, assets, and expertise of the private sector to scale humanitarian operations, ensuring aid reaches those who need it most, when it matters most.”

Behind the statistics and logistics operations are real people whose lives have been transformed by the LET’s work. Here are just some of the ways the Logistics Emergency Team has responded to crises over the past 20 years:

- Gaza crisis response

Since the opening of the Jordan corridor in November 2023, the LET has been instrumental in the Gaza humanitarian response. The partnership provided a fully equipped and staffed warehouse in Amman, Jordan, strategically positioned to consolidate aid before dispatch into Gaza. Since the warehouse opened in July 2024, 28,915 cubic meters of cargo from 21 humanitarian organizations have been processed for consolidation.

- Ukraine crisis support

In February 2022, the LET companies activated their presence around Ukraine to provide warehouse space and ground transportation for humanitarian supplies. The partnership’s existing regional infrastructure and local knowledge proved invaluable in streamlining aid distribution to affected areas. The LET provided crucial customs clearance information and facilitated the humanitarian supply chain along the Poland-Ukraine border.

- Türkiye-Syria earthquake response

Following the devastating 7.8 magnitude earthquake that struck Türkiye and Syria in February 2023, killing over 50,000 people, the LET rapidly deployed comprehensive support. The LET companies provided customs clearance, local transportation market assessment and in-country transportation as well as funding to the Logistics Cluster for the overall response. LET members facilitated an airlift from the UN Humanitarian Response Depot in Brindisi, Italy, to Adana, Türkiye, and offered access to local logistics experts and mobile storage units.

By Tarek Sultan

Vice-Chairman of the Board, Agility

- Investment is pouring into Gulf startups from domestic and foreign sources.

- Start-up friendly policies, access to funding and the multiplier effect are just a few of the reasons for this growth in investment.

- Powerful local and global economic currents are benefitting the Gulf states.

This is a golden age for startups and entrepreneurs in the six countries of the Gulf Cooperation Council (GCC). Geopolitics, technology, climate urgency and daring national agendas across the region have combined to create what might be the most favourable conditions that small businesses anywhere have ever enjoyed.

Private-sector expansion is the key to national ambitions in all six countries. Increasingly, Gulf leaders will be looking to small business and entrepreneurs as engines of job creation and innovation.

The time is right. The ecosystems that Gulf countries established to nurture, fund and scale digital startups are maturing. Gulf funders — from sovereign wealth funds to venture capitalists to family offices — are looking to write checks to entrepreneurs closer to home. Regulatory fine-tuning is creating new openings for smaller companies that have struggled to compete. Massive infrastructure, energy and technology projects are having a spinoff effect for local businesses and specialized service providers. Finally, powerful currents in Gulf trade, foreign investment, research and e-commerce are all working in favour of SMEs.

Five reasons the time is now for startups and small businesses in the Gulf

1. Funding

Simply put, there’s more money from local and international sources looking to invest in young, innovative Gulf companies.

The Gulf’s sovereign wealth funds have more than $4 trillion in assets under management, a record. They account for more than 40% of global SWF wealth, and their investments comprised 40% of the global sovereign investment total through the first nine months of 2024. Increasingly, Gulf fund managers are looking to invest more at home so that they can drive private-sector growth at the heart of the region’s national strategies.

Saudi Arabia’s Public Investment Fund (PIF) is shifting the balance of its portfolio to focus less on international holdings and more on investment in new industries and projects in the Kingdom. PIF Governor Yasir Al-Rumayyan said in October that the fund will trim its global holdings to 18% of its portfolio, down from 30% in 2020.

In other cases, Gulf sovereign funds are putting money into young companies with innovative ideas that can aid home-country economic diversification. Abu Dhabi’s Mubadala recently invested in Odoo, a Belgian company that offers single-platform software for small and medium-sized companies.

Venture capital investment in the GCC quadrupled from 2017 to 2022 and continues to outpace growth in most other geographies, increasing at a 24% compound annual growth rate. Investment is pouring into Gulf startups in AI, specialized online marketplaces, climate tech, delivery apps, fintech, edtech and investment platforms.

At the same time, overseas funds such as US-based ScienceWerx are putting down new roots in Saudi Arabia and neighboring countries so they can be first movers in AI, biotech, healthtech and other emerging fields. Similarly, Brookfield Asset Management says it is raising at least $2 billion for a new Middle East-focused private equity fund with PIF and other partners.

2. Multiplier effects

The vast majority of small businesses in the Gulf aren’t the kind to attract direct investment from sovereign funds and venture capitalists. But most can expect to be lifted by the “agglomeration” or multiplier effect that flows from the staggering amount of investment and spending across the region, particularly in mega-projects, logistics infrastructure, AI, clean energy and climate adaptation.

In the US, where most of the research on multiplier effects has been done, there is a clear correlation between investment and increased demand for local goods and services; increased productivity; and job creation. The addition of one highly skilled job in an urban area creates 2.5 jobs in other sectors dominated by smaller businesses: construction, food service and other localized roles.

3. Regulatory incentives

Gulf governments are using their policy levers to create new jobs, expand private-sector growth and boost investment. Among all the carrots and sticks being deployed by policymakers are loads of advantages and opportunities that benefit smaller businesses. Some examples:

— In the UAE, where there are nearly 50 economic free zones, operators are competing to create the most business-friendly conditions. The Ajman NuVentures Centre Free Zone, the newest in the Emirates, promises to grant business licenses online in 15 minutes and issue two-year visas for investors within 48 hours.

— In Saudi Arabia, one of the main drivers of growth in the small business sector has been the Kingdom’s sweeping push to make it easier and more attractive for women to join the workforce. Since 2017, the Kingdom has lifted the ban on women driving, introduced anti-harassment laws, expanded female legal autonomy, introduced childcare and transportation subsidies for working women, mandated equal pay and prohibited termination of pregnant women. Today, women own 45% of small and medium-sized businesses in Saudi Arabia. The rate of female participation in the labour force roughly doubled to 35% between 2017 and 2023.

— To create jobs for their citizens, Gulf countries are requiring private companies to meet hiring quotas and maintain a certain percentage of nationals in their workforce. In the UAE, small businesses can qualify for grants, subsidies and reduced fees by taking part in labour force Emiratization.

— Saudi Arabia’s Regional Headquarters Programme, intended to get multinationals to establish their regional head offices in the Kingdom, will add to the multiplier effect by sending global companies in search of Saudi partners for everything from local recruiting to branding, advertising and marketing.

4. Promotion and skills development

Gulf countries are getting better at figuring out what startups and small businesses need. Where non-energy exports used to be negligible, they are now aggressively promoted by the Saudis, Emiratis and other GCC governments.

In Kuwait, which licensed 6,700 new companies through the first three quarters of 2024, the National Fund for SME Development recently launched its Mubader Plus programme, offering workshops, counseling and other assistance to budding entrepreneurs.

Dubai’s Expand North Star, with 70,000 in attendance in 2024, is the world’s largest tech startup and investment event.

5. Powerful tailwinds

Gulf leaders are embracing the post-World War II US innovation model, which uses government money to fund university research that can produce ideas later scaled and commercialized by the private sector. GCC countries are establishing or expanding universities and pushing them to innovate through partnerships with leading international research institutions or alongside Gulf counterparts through platforms such as the Qatar-led My Gulf University.

Trade trends are also working in favour of SMEs. The UK and six GCC countries are nearing completion of a new free trade agreement valued at $73 billion annually. A new FTA with the UK is likely to accelerate economic integration among the six countries, as will Gulf e-commerce, which continues to outpace other regions in annual growth.

Not to be overlooked is the China factor. Chinese companies are looking to the Gulf as the place where they can diversify their manufacturing base, invest in renewable energy and hydrogen production and become EV market share leaders. Chinese investment in Gulf-based AI and tech development is making the GCC a hub for digital transformation and commerce.

For entrepreneurs, startups and small business in the GCC, it’s never been a better time.

This blog was originally published by the World Economic Forum.

As the Future Investment Initiative (FII) Conference convenes in Riyadh in October 2024, we are premiering a mini-documentary that highlights the pivotal role logistics plays in Saudi Arabia’s bold Vision 2030 transformation.

Featuring exclusive footage from the Global Logistics Forum, the film captures industry leaders describing how the Kingdom is emerging as a global logistics hub. It also showcases Agility’s expanding operations in Saudi Arabia, underscoring our commitment to supporting a diversified, sustainable economy.

By Tarek Sultan

Vice Chairman, Agility

- While advancements in renewable energy sources like solar and wind are significant, the infrastructure and market aren’t fully prepared to abandon fossil fuels immediately.

- Bridge solutions, such as natural gas and nuclear power, are needed to ensure energy security and economic stability during the clean energy transition.

- More collaborative efforts between the public and private sectors would be beneficial in developing practical regulations that encourage investment without stifling innovation.

Powering the grid

Power generation is the leading source of carbon dioxide emissions. The International Energy Agency recently sent hearts aflutter with the news that “unstoppable” low-carbon technologies have global fossil fuel use on track to peak much earlier than expected – by 2025 or before. According to the International Energy Agency, four-fifths of the new power capacity being added today is generated by renewables.

That’s encouraging but the fact remains that our electrical grid is not yet renewable-ready and that roughly 80% of our power is still supplied by fossil fuels. Our ability to continue adding capacity from solar, wind and other alternatives is limited unless we progress on the hard, time-consuming and expensive task of extending or adding transmission lines and costly infrastructure.

Moreover, some key assumptions underlying earlier forecasts are no longer valid. Power demand is not static. It is surging as we put more electric vehicles on the road, build new data centres and add semi-conductor manufacturing capacity. Chip factories and data centres consume 100 times more power than typical industrial businesses.

Bridging the energy transition

Even with added solar and wind generation, we’ll need reliable new baseload power sources to replace what we get today from fossil fuels. That’s why there is so much interest in scaling and commercializing clean hydrogen.

In the meantime, however, we need “bridge” solutions. Natural gas and nuclear power are cleaner than coal and oil. While both are environmentally problematic, we risk damaging the global economy and threatening our energy security if we cut them off prematurely without using them to aid our transition.

Political opposition is blocking investment in new natural gas infrastructure – pipelines, liquefaction facilities, shipping – when we could invest in ways to reduce LNG methane emissions by mitigating leaks associated with drilling, storage and transport.

Earthmind’s Franklin Servan-Schreiber makes the case for the growing importance and viability of nuclear power, particularly in the Gulf. Advances in “transmutation” nuclear energy processes make it possible to generate power in a way that is safer, cleaner and cheaper while also addressing fears of nuclear weapons proliferation.

“Nuclear energy represents the only carbon-free baseload energy available in this (Gulf) region without rivers, making it an indispensable component of any net-zero energy mix,” says Servan-Schreiber.

Increase in deployment of climate technologies needed to reach emissions reduction targets by 2030, from 2021.Image: McKinsey

On the road

In road transportation, zero-carbon solutions are being considered but are not practical today. And that’s not all bad: the “greenest” car in America isn’t a fully electric Tesla or Rivian. It’s the trusty hybrid Toyota Prius, which is hugely popular, versatile, reliable and affordable.

Sadly, there are few hybrid options when it comes to long-haul trucking. The bulk of research and development and investment have gone toward developing emissions-free vehicles: battery-electric and hydrogen-fuel trucks.

For now, trucks powered by heavy, industrial-scale batteries have a maximum range of about 300 miles and require several hours to recharge. Hydrogen-powered trucks refuel faster (about 30 minutes) and can cover up to 500 miles at a time. In both cases, adequate fueling networks and infrastructure are years away. In the meantime, current versions of zero-emission vehicles are still roughly three times more expensive than diesel trucks, even after tax breaks and incentives.

In business

On the policy front, businesses are struggling to keep pace with new emissions mandates and disclosure requirements. This year, new reporting rules in Canada and Germany prompted howls of protest from businesses begging for more time to comply. The EU recently rejected new rules requiring detailed reporting on the environmental and labour impacts of member countries’ supply chains.

Elsewhere, companies have retreated from their climate commitments and struggled to persuade investors that sustainability investment will be rewarded with returns.

“Access to capital for new low-carbon investments isn’t a major constraint, but ensuring a return on investment certainly is,” stated Bain & Co. in a September report on the energy transition.

The pushback from business highlights the importance of more collaboration between the public and private sectors. Business leaders recognize the need for environmental and sustainability standards that will advance the net-zero agenda. However, they also want to ensure that new guidelines and mandates don’t crowd out investment or undermine new technology before it can be fully developed.

Accept our marketing cookies to access this content.

These cookies are currently disabled in your browser.Accept cookies

Prioritizing resilience

More than 40 countries – home to about half the global population – will hold elections this year. To some extent, the voting will be a referendum on climate policies that are increasingly shaping everyday life. Politicians and policymakers need to counter apathy and climate fatigue with information that brings home the urgency of our transition. But to avoid a popular backlash, we need to avoid fixating on zero-carbon technologies at the expense of low-carbon tech that is cheaper and can deliver immediate impact at a fraction of the cost.

That also means that we can’t allow our pursuit of a zero-carbon future to prevent us from investing in adaptation and resilience. Even if we’re able to accelerate the energy transition, we need to spend money on seawalls, stormwater management, water supply, distributed power grids, and weatherized buildings, homes and power infrastructure.

The clean energy revolution is paying dividends every day, though not always in the way we expect. Technological refinements are bringing us closer to a carbon-free future. Still, companies that set out to do one thing sometimes end up doing another, as in the case of Molten Industries. This hydrogen startup invented a new way to produce graphite, which is used to expand battery storage capacity.

It’s not a matter of lowering our sights or settling for the incremental over the transformative. We need both.

This blog was originally published on 24 April 2024 at Weforum.org. Read the original article here.

By Tarek Sultan

Vice Chairman, Agility

- Overall, we are not acting fast enough to cut fossil fuels and make the climate transition a reality, but there is reason to be optimistic, too.

- Policies are changing faster than anyone expected, and solar power’s proliferation appears unstoppable.

- Fossil fuels look more and more like a stranded asset, while investments in renewables are increasingly good bets.

Every day, we get a clearer picture of the threat from a warming planet and the costs we incur amid the transition to clean energy and a low-carbon future.

It’s easy to be discouraged in the face of the largest-scale challenge humanity has ever collectively faced: tackling climate change and preventing warming above 1.5°C.

In recent months, we’ve heard fresh doubts about electric vehicle demand, seen fossil fuel production increases and private-sector oil investments that fly in the face of climate pledges. The market for shares of clean energy companies has been depressed, and there are signs of a backlash against emission-reduction policies.

Accenture’s analysis of the top 2,000 global companies shows that only 37% are committed to achieving net zero by 2050 — and just 18% are on track reach that goal. Businesses are struggling to afford decarbonization and CEOs are pessimistic about hitting the UN’s Sustainable Development Goals.

But hitting net zero by 2050 was never going to be easy — and it is apparent that there is a historic change happening. By some measures, it is now unstoppable.

The climate transition tipping point

The International Energy Agency (IEA) says that fossil fuel demand will peak by 2030. Renewables will overtake coal as the leading source of electricity by 2025. Solar and wind power, both now cheaper than ever, generate more than 10% of electricity and account for 75% of new power-generating capacity. We may have already passed a tipping point at which it is inevitable that solar energy will come to dominate electricity markets.

In road transport, electric vehicles have grown to 15% of new vehicle sales, and the range of the average EV has tripled over the past 10 years.

What’s more, a number of potential gamechangers are on the cusp of broad commercialization: renewable-energy technologies, electric mobility alternatives, heat pumps for zero-carbon home heating, carbon capture and storage, green hydrogen fuels and industrial electrification. In Europe alone, those technologies could address up to 45% of the greenhouse gas abatement required for net zero, McKinsey says.

The pace of the energy transition will largely be decided by China, the United States and the European Union — the world’s biggest greenhouse gas emitters. China’s emissions are set to peak by 2030. In the US, a rapid transition is underway.

There are hopeful indicators in other economies, as well. Brazil and Indonesia have taken steps to halt deforestation and some other countries have declared that they will leave their oil and gas reserves in the ground.

Overcoming obstacles through innovation

Of course, the energy transition demands constant and rapid innovation. Of late, we’re seeing the power of human creativity brought to bear on some of the climate transition’s toughest challenges: materials shortages, production bottlenecks, risk mitigation and financing.

The shift to electric vehicles has highlighted the difficulty in securing adequate supplies of lithium and rare earth minerals used in batteries. But it also has triggered a search for substitutes such as wood chips — a source of synthetic graphite for electric vehicles— and heightened the realization that the energy transition is a materials transition.

Similarly, hydrogen-powered heavy haul trucks are emerging as an alternative to battery-cell rigs. New alternatives in textiles and construction are being scaled. Innovations in recycling are making steel, plastics and cement cleaner, more versatile and more durable.

Adoption of green energy for road transport and ocean shipping is farther along than in commercial aviation, but in November, Virgin Atlantic completed the first transatlantic commercial flight fully powered by sustainable aviation fuel. Elsewhere, fertilizer producers are making strides in solving the production and storage problems associated with producing low-carbon ammonia for fuel.

Global investors have doubled their investment in transition technologies from $660 billion in 2015 to more than $1 trillion today. Climate-related venture capital investment increased 89% from 2021 to 2022. Advance market commitments — binding contracts by governments, development banks and others to guarantee a viable market for a product — are spurring innovation and bridging the gap needed to complete successful development of green products and services.

The policy environment: changing fast

We shouldn’t require any reminders about the urgency of the climate challenge: 2023 was the hottest year on record and 2024 is forecast to be even warmer with the arrival of El Niño.

Historically, it’s usually been safe to bet on government and policy inertia. But climate policies and legislation are getting bolder, and there appears to be more fast-tracking than backtracking. A review of 215 policies across two dozen major economies since 2015 found 17 examples of backtracking and 41 of accelerated action with most others unchanged. The review predicted a public clamor for speedier climate action as extreme weather exacts a heavier toll and green tech shows increasing promise.

At the same time, there is growing determination to develop better green standards and to buffer developing economies and vulnerable populations from the effects of a costly and disruptive transition by offering technical and financial assistance.

At COP28, the agreement to cut down on greenhouse gas emissions from methane was a major victory. Less certain is the immediate impact of language about a “transition away” from fossil fuels. COP’s statement on oil, gas and coal was not strong enough for many environmental advocates, but it did mark a breakthrough.

As Jennifer Morgan, Germany’s climate envoy, said: “Every investor should now understand that future investments that are profitable and long-term are renewable energy — and investing in fossil fuels is a stranded asset.”

This blog was originally published on 04 January 2024 at Weforum.org. Read the original article here.

- Female-founded companies received only 2% of all venture capital (VC) investment in 2022.

- Gender bias and a scarcity of female investors are thought to hamper VC investment in female-owned businesses.

- By expanding female-led VC communities, highlighting successful VC funding for female businesses and confronting stereotypes, more VC funding should flow to female-founded companies.

By most measures, women are making steady gains in professional opportunity, pay and status and decision-making power at work. Their progress, while slow and uneven, is reflected in economic empowerment indexes put out by the OECD, World Health Organization, UN agencies and others.

One area where women are advancing little, however, is venture capital (VC). Companies founded solely by women received only 2% of all VC investment in 2022, and only about 15% of all VC ‘cheque-writers’ are women.

In the Middle East, where my company is based, venture capital investment is increasingly seen as a critical component of national economic competitiveness and a source of innovation. The region’s VC funds and corporate VCs are competing with sovereign wealth funds, among the world’s largest and most active VC investors. Yet, startups founded by women in the Middle East and North Africa (MENA) received only 1.2% of funding in 2021 and about 2% last year.

Image: Data Source: McKinsey

Image: Data Source: McKinsey

What’s behind the disparity?

The glaring imbalance has sparked lively debate about what’s causing it.

Venture capital is a male-dominated industry and bias, whether conscious or subconscious, is clearly a factor. A Harvard study showed that 70% of VC investors preferred pitches presented by male entrepreneurs over those presented by female entrepreneurs, even though the pitches were identical.

Another analysis has shown that VC investments in enterprises founded or co-founded by women average less than half the amount invested in companies founded by male entrepreneurs.

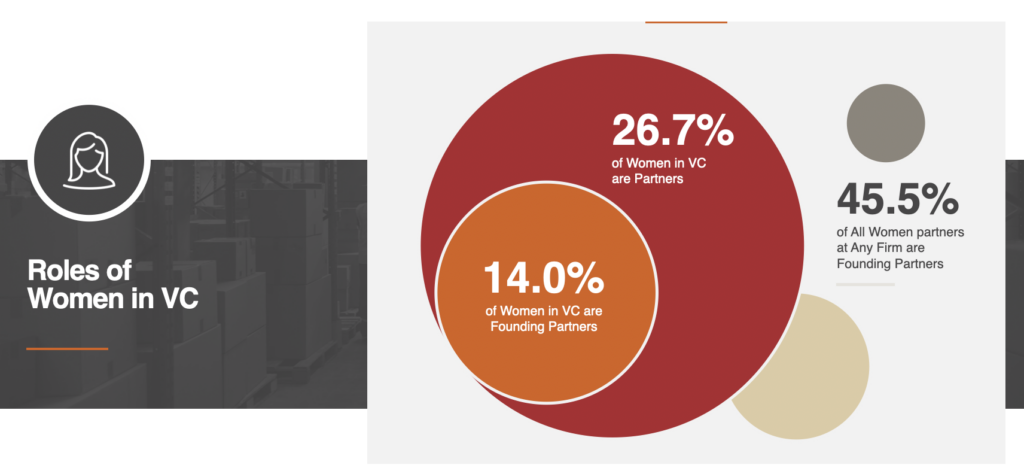

Image: Data Source: Women in VC

In Inc.’s Women Entrepreneurship Report, 62% of female entrepreneurs said they experienced some form of gender bias during the funding process. Feelings of bias are especially acute among women entrepreneurs in MENA. In a survey of 125 female founders in the region, 58% said MENA investors were less likely to invest in women-led startups than global investors.

The scarcity of female investors – those who sit on fund boards, lead deals, and make investment decisions – is also an issue. However, the authors of a Harvard Business Review article on the VC gender gap caution women founders against focusing solely on pitching to female investors.

“There are still very few female investors, and they tend to be concentrated in funds that focus on earlier-stage investments, where risk is higher and funds invested are smaller. Today, female VCs simply do not control sufficient assets to continue investing in female-led firms as they scale. This means that female founders will ultimately need to attract male investors to grow — and if you’re a woman, our research shows that’s a lot easier to do if you raise at least some capital from men from the start,” they wrote.

Another hard reality is the lack of a pipeline; here I speak from experience. Our corporate VC arm, Agility Ventures, received about 1,000 pitch decks last year. How many came from women-founded or women-led businesses? I can count them on one hand.

The lopsided numbers in MENA are especially perplexing because of the inroads women in the region have made in the educational fields that generate most of the innovation and ideas sought by venture investors. Women now account for 57% of STEM students at MENA universities, according to UNESCO.

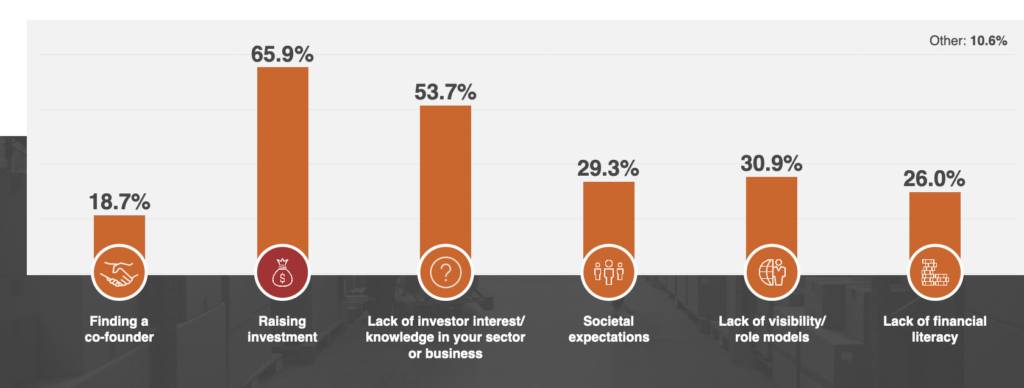

What do you think are the biggest obstacles facing women founders?Image: Data Source: Wamda, TiE Dubai – survey of 125 female founders in MENA, published in collaboration with TiE Dubai and TiE Women

Why address the VC gender gap?

Apart from the need to address basic inequity, there are plenty of reasons to tackle the gender chasm in venture capital. The biggest is the chance to unlock economic gains.

Venture funding de-risks the innovation process through bets on promising ideas from smart people who need resources to get their ideas to market. It’s a wellspring of new technology, business growth and economic development, which makes the diversity of entrepreneurship and VC leadership economic imperatives. A widely cited BCG report says global GDP would rise 3% to 6%, boosting the global economy by up to $5 trillion annually if women entrepreneurs received the same investment as male entrepreneurs.

Accept our marketing cookies to access this content.

These cookies are currently disabled in your browser.Accept cookies

What’s the answer?

Expand women-led VC communities

That means networking, mentorship, technical assistance and other support. It means building on the work of investment community participants, such as Women in VC, the world’s largest global community for women in VC to connect and collaborate; AllRaise, an organization dedicated to accelerating the success of women founders and funders; and the Female Founders Fund, an early-stage fund that offers pitching resources and technical help in addition to investing in women-led tech startups.

It also means more non-profit and public-sector programmes, such as empowerME, an initiative aimed at female entrepreneurs in the Middle East; Monsha’at, a Saudi government small business authority with an entrepreneurship programme targeted at women; She Innovates, the global UN Women programme that connects female innovators via app and platform; and Global Invest in Her, a platform for women entrepreneurs seeking funding.

Celebrate success

We need to elevate the visibility of female role models who have raised capital and successfully brought products and services to market. Stories of success act as inspiration and provide models for females in business to emulate. Mona Ataya, CEO of Mumzworld, is a good example.

Confront stereotypes

The Global Entrepreneurship Monitor (GEM) highlights one damaging stereotype: that businesses started by women typically aren’t the kind that are right for outside investment because they’re low-tech enterprises in sectors with little potential to scale, trade across borders and go public through stock offerings.

“More attention needs to be given to women who are starting and growing high growth, high innovation and large market businesses. Stereotypes that frame women entrepreneurs as a disadvantaged group feed a false narrative that women lack the same competency as men regarding business leadership,” the GEM team says.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

By Agility Vice Chairman Tarek Sultan

As I head to Saudi’s FII conference, known as “Davos in the Desert” this week, I am reflecting on the pace of change I’ve personally witnessed in KSA.

Saudi Arabia’s progress in its journey to becoming a Tier 1 global logistics hub has been impressive. It’s clear the Kingdom is already ahead of many key targets and on course to meet many more, diversifying its economy and enhancing its global profile.

Agility has been investing in Saudi Arabia for 20 years. The scale, resources, resolve, and pace of reform we have seen in Saudi Arabia in recent years has been particularly exciting. In our view, Saudi Arabia is one of the most attractive markets for logistics investments in the world today.

Agility is investing in KSA around the following areas:

- Building essential infrastructure. We’re building a world-class logistics and distribution park near Jeddah. We’ve committed SAR 611 million ($163 million) to the 570,000 SQM project, an ultra-modern facility to go with the state-of-the-art Agility Logistics Parks already serving Saudi companies and multi-nationals in Riyadh and Dammam.

- Improving Air Travel. Our Menzies Aviation business is the world’s largest aviation services company. It has partnered with Saudi Logistics Services (SAL) to improve passenger services, cargo handling and warehousing, and airline hub management for Saudi-based airlines.

- Speeding the low-carbon transition. The Agility Logistics Park in Riyadh features the GCC’s first EDGE Advanced-certified warehouse (Excellence in Design for Greater Efficiencies), meaning it is zero-carbon ready and at least 40% more energy efficient than others in the market. Tristar also is building the Kingdom’s first LEED-certified green building for dangerous goods (DG), in Modon Dammam Second Industrial City.

- Investing in Saudi innovation. Through our venture capital arm, Agility Ventures, we have invested in Saudi Arabia’s entrepreneurs and digital innovators, such as e-commerce enablement innovator Zid and digital road freight platform Humoola. We are also helping bring transformational global health technologies to the Kingdom, through partnerships with companies like AiZTech Labs, which has developed breakthrough medical testing using selfies of the eyes taken with mobile phones and Bexa, a company pioneering innovative breast cancer screening technologies.

- Powering e-commerce. Our Shipa group of companies include Shipa Delivery, one of the Kingdom’s most advanced last-mile delivery providers, and Shipa E-Commerce, a leader in cross-border fulfillment. Shipa provides both domestic parcel delivery and cross-border shipping to and from the GCC and Saudi Arabia.

- Enhancing energy-sector efficiency and safety. Agility affiliate Tristar Group works with Aramco, SABIC, and others in the energy sector to modernize equipment, vehicles and storage facilities used in the handling of chemicals, cryogenic gases and hazardous goods — essential industrial feedstocks.

- Strengthening Saudi companies. United Stars, Tristar’s Saudi JV, earned the highest score among multi-nationals in Aramco’s In Kingdom Total Value Add (iktva) program. The program’s goal is to build a world-class supply chain while cultivating local business and retaining at least 70% of all procurement spend within the Kingdom. United Stars focuses on recruiting, coaching and developing strong Saudi teams.

When it comes to Saudi Arabia’s growth potential, Agility is an investor, partner, and supporter.

As I head to Saudi’s FII conference, known as “Davos in the Desert” this week, I am reflecting on the pace of change I’ve personally witnessed in KSA.

Saudi Arabia’s progress in its journey to becoming a Tier 1 global logistics hub has been impressive. It’s clear the Kingdom is already ahead of many key targets and on course to meet many more, diversifying its economy and enhancing its global profile.

Agility has been investing in Saudi Arabia for 20 years. The scale, resources, resolve, and pace of reform we have seen in Saudi Arabia in recent years has been particularly exciting. In our view, Saudi Arabia is one of the most attractive markets for logistics investments in the world today.

Agility is investing in KSA around the following areas:

- Building essential infrastructure. We’re building a world-class logistics and distribution park near Jeddah. We’ve committed SAR 611 million ($163 million) to the 570,000 SQM project, an ultra-modern facility to go with the state-of-the-art Agility Logistics Parks already serving Saudi companies and multi-nationals in Riyadh and Dammam.

- Improving Air Travel. Our Menzies Aviation business is the world’s largest aviation services company. It has partnered with Saudi Logistics Services (SAL) to improve passenger services, cargo handling and warehousing, and airline hub management for Saudi-based airlines.

- Speeding the low-carbon transition. The Agility Logistics Park in Riyadh features the GCC’s first EDGE Advanced-certified warehouse (Excellence in Design for Greater Efficiencies), meaning it is zero-carbon ready and at least 40% more energy efficient than others in the market. Tristar also is building the Kingdom’s first LEED-certified green building for dangerous goods (DG), in Modon Dammam Second Industrial City.

- Investing in Saudi innovation. Through our venture capital arm, Agility Ventures, we have invested in Saudi Arabia’s entrepreneurs and digital innovators, such as e-commerce enablement innovator Zid and digital road freight platform Humoola. We are also helping bring transformational global health technologies to the Kingdom, through partnerships with companies like AiZTech Labs, which has developed breakthrough medical testing using selfies of the eyes taken with mobile phones and Bexa, a company pioneering innovative breast cancer screening technologies.

- Powering e-commerce. Our Shipa group of companies include Shipa Delivery, one of the Kingdom’s most advanced last-mile delivery providers, and Shipa E-Commerce, a leader in cross-border fulfillment. Shipa provides both domestic parcel delivery and cross-border shipping to and from the GCC and Saudi Arabia.

- Enhancing energy-sector efficiency and safety. Agility affiliate Tristar Group works with Aramco, SABIC, and others in the energy sector to modernize equipment, vehicles and storage facilities used in the handling of chemicals, cryogenic gases and hazardous goods — essential industrial feedstocks.

- Strengthening Saudi companies. United Stars, Tristar’s Saudi JV, earned the highest score among multi-nationals in Aramco’s In Kingdom Total Value Add (iktva) program. The program’s goal is to build a world-class supply chain while cultivating local business and retaining at least 70% of all procurement spend within the Kingdom. United Stars focuses on recruiting, coaching and developing strong Saudi teams.

When it comes to Saudi Arabia’s growth potential, Agility is an investor, partner, and supporter.